Understanding Business Restructuring in Transfer Pricing

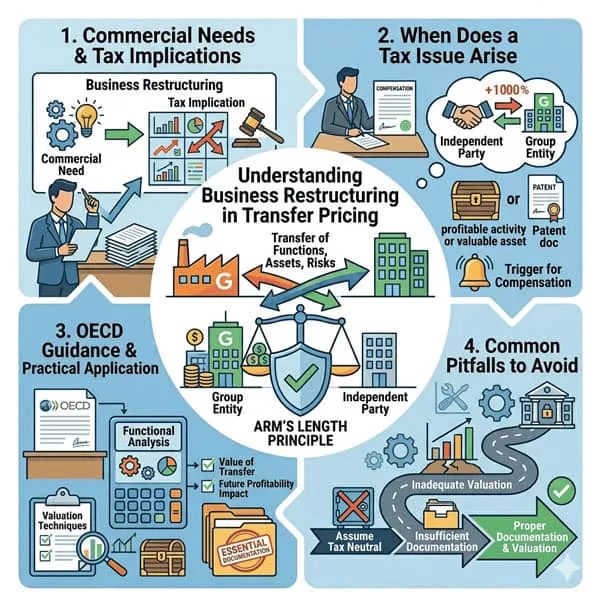

Business restructurings are often driven by commercial needs, but they can have significant tax implications.

Any transfer of functions, assets, or risks within a group must be assessed under the arm’s length principle.

When Does a Tax Issue Arise

The key question is whether an independent party would have required compensation for the transfer.

For example, transferring a profitable activity or valuable asset may trigger a need for compensation between group entities.

OECD Guidance and Practical Application

Under OECD guidance, the analysis focuses on the value of what is being transferred and the impact on future profitability.

This requires a combination of functional analysis and valuation techniques.

Common Pitfalls

Businesses often assume that internal reorganisations are tax neutral. In practice, this is rarely the case.

Proper documentation and valuation are essential to support the position taken.